If you are an NRI earning income from Indian mutual funds, fixed deposits, NRO accounts, or stocks chances are you are already paying tax in India. But here is the part most NRIs miss: your country of residence (USA, UK, Canada, Australia) may ALSO tax that same income. This is called double taxation and without the right planning, you could lose 30%–40% of your investment returns to two different tax authorities simultaneously.

The good news? India has signed Double Taxation Avoidance Agreements (DTAA) with 90+ countries and if you know how to use them, you can legally avoid double taxation on NRI investments and keep more of what you earn. This 2026 guide explains exactly how to do that step by step.

What Is Double Taxation for NRI Investments?

Double taxation means the same income gets taxed in two different countries. For NRIs, this happens because:

- India taxes income at source:- Any income you earn from Indian investments interest, dividends, capital gains is taxable in India because it originates here.

- Your resident country taxes global income:- Countries like the US, UK, Canada, and Australia require their tax residents to report and pay tax on worldwide income including what they earn in India.

How DTAA Helps Avoid Double Taxation on NRI Investments

India has signed Double Taxation Avoidance Agreements (DTAA) with over 90 countries. These are legal treaties that decide which country gets to tax your income and by how much.

| DTAA Method | How It Works | Best For |

| Exemption Method | Income taxed only in ONE country. The other country fully exempts it. | UAE NRIs (no income tax in UAE) |

| Tax Credit Method | Tax paid in India is credited against your home country tax bill. | US, UK, Canada NRIs |

| Reduced TDS Rate | DTAA lowers India’s TDS rate below the standard 30%. | Interest income, dividends |

Country-Wise DTAA Snapshot for NRI Investors (2026)

| Country | TDS on Interest (DTAA Rate) | Capital Gains Tax | Key Benefit |

| USA | 15% (vs 30% standard) | India can tax | FTC claim on IRS return |

| UK | 15% (vs 30% standard) | India can tax | FTC claim with HMRC |

| Canada | 15–25% | India can tax | FTC against CRA |

| UAE | Exempt in many cases | India can tax | No UAE income tax — max savings |

| Singapore | 15% | Limited after 2017 | Reduced TDS on interest |

| Australia | 15% | India can tax | FTC on Australian return |

NRI Investment Types Tax Rules & Double Taxation Risk

Not all NRI investments are taxed the same way. Here is a breakdown of how different investment types are affected and what you can do to avoid double taxation on NRI investments:

1. NRO Fixed Deposits & Savings Accounts

- TDS Rate in India:- 30% (standard) | Can be reduced via DTAA to 10–15%

- Risk:- Interest fully taxable in India + must be declared in home country

- Solution:- File Form 10F + Tax Residency Certificate (TRC) with your bank to claim reduced DTAA rate

2. Mutual Funds & Stocks — Capital Gains

| Type | Holding Period | India Tax Rate (2026) | Double Tax Risk |

| STCG (Equity Funds/Stocks) | Less than 12 months | 20% | High — taxable in both countries |

| LTCG (Equity Funds/Stocks) | More than 12 months | 12.5% above ₹1.25 lakh | Medium — FTC can offset |

| STCG (Debt Funds) | Less than 24 months | As per slab rate | High |

| LTCG (Debt Funds) | More than 24 months | As per slab rate | Medium |

Important 2026 Update: Debt mutual funds no longer get indexation benefits. All gains are now taxed at slab rates regardless of holding period. NRIs must plan carefully to avoid excessive double taxation.

3. NRE Account Interest

- India Tax:- Fully EXEMPT, NRE account interest is tax-free in India

- Home Country Tax:- Taxable in USA, UK, Canada etc. as foreign interest income

- Solution:- Declare on your home country return. Use DTAA credit if India taxes any related income.

4. Indian Stock Dividends

- India TDS:- 10% TDS on dividends exceeding ₹5,000 per company

- DTAA Rate:- Can be reduced to 10–15% under applicable treaty

- Solution:- File TRC + Form 10F with depository/company registrar before dividend credit

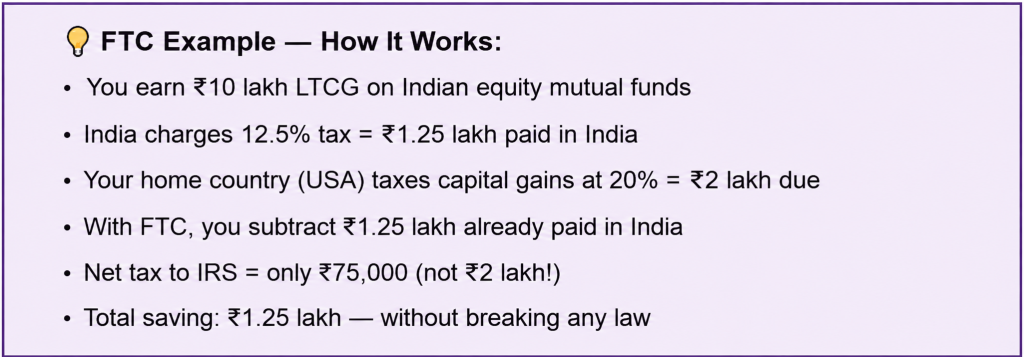

Foreign Tax Credit (FTC) — The Most Powerful Tool to Avoid Double Taxation

Even after DTAA, there may be situations where both countries tax your income. In that case, the Foreign Tax Credit (FTC) is your most powerful weapon.

FTC allows you to subtract the tax already paid in India from your home country’s tax bill on the same income.

How to Claim FTC — Country Wise

| Country | FTC Form / Method | Deadline |

| USA | IRS Form 1116 — Foreign Tax Credit | With your annual 1040 return |

| UK | SA106 — Foreign Income page | Self Assessment deadline |

| Canada | T2209 — Federal Foreign Tax Credits | With T1 General return |

| Australia | Foreign Income Tax Offset (FITO) in Tax Return | Annual ITR deadline |

⚠️ Critical Rule: To claim FTC in India’s ITR, you MUST file Form 67 before the ITR due date. Missing this = losing your credit claim.

Step-by-Step: How to Claim DTAA Benefits on Your NRI Investments

Step 1. Get Your Tax Residency Certificate (TRC): Obtain from your foreign country’s tax authority. Example: IRS Form 6166 for USA, HMRC clearance for UK. This proves you are a tax resident of that country.

Step 2. File Form 10F Online: Submit electronically on India’s e-filing portal (incometax.gov.in). Required if your TRC does not have all mandatory fields. Must be done BEFORE the income is received.

Step 3. Submit Documents to Your Bank/Broker: Give your TRC + Form 10F to your Indian bank (for NRO FD interest) or broker (for dividend/capital gains). They will apply a reduced DTAA TDS rate instead of 30%.

Step 4. File Indian ITR: Report all Indian income in your ITR (ITR-2 for NRIs). Claim any excess TDS as refund. Include Form 67 if claiming FTC.

Step 5. File Your Home Country Return: Declare Indian income. Attach proof of Indian taxes paid. Claim FTC using the appropriate form for your country.

Documents Required to Avoid Double Taxation on NRI Investments

| Document | Purpose | Where to Get It |

| Tax Residency Certificate (TRC) | Proves you are a tax resident of foreign country | IRS (USA) / HMRC (UK) / CRA (Canada) |

| Form 10F (Electronic) | Self-declaration to validate TRC in India | incometax.gov.in portal |

| PAN Card (Active) | Mandatory for all Indian transactions. Without it, 20% higher TDS | NSDL / UTI portal |

| Form 67 | Required to claim FTC in Indian ITR | Income Tax e-filing portal |

| TDS Certificates (Form 16A) | Proof of tax deducted in India (for FTC claim abroad) | Your Indian bank or broker |

| ITR Acknowledgement | Proof of Indian tax filing — needed by some foreign countries | Income Tax e-filing portal |

Costly Mistakes NRIs Make — And How to Avoid Them

- Not submitting TRC + Form 10F to the bank:- Result: Bank deducts 30% TDS instead of 10–15% DTAA rate. You lose cash flow immediately.

- Not reporting Indian income in home country return:- Result: IRS/HMRC penalties for undisclosed foreign income. Risk of audit and heavy fines.

- Missing Form 67 deadline: Result: FTC claim rejected entirely. You pay full tax in both countries with no relief.

- Confusing NRE and NRO accounts:- Result: NRE interest is tax-free in India but taxable abroad. NRO interest is taxable in India. Mixing these up = wrong ITR filing.

- Not filing Indian ITR at all:- Result: Excess TDS stuck with Income Tax department. No refund possible without ITR filing.

- Using an India-only CA for cross-border taxes:- Result: CA may not know your home country’s FTC rules. You need a cross-border NRI tax specialist.

Related Guides You Should Read Next

How Can I Avoid Double Taxation On Property Sale As An Nri?

How to File Income Tax Return for NRI – Full Guide 2026

The Ultimate US Tax Filing Guide for NRIs 2026

NRI Tax Filing Services in India: Complete Guide for NRIs

Conclusion

Avoiding double taxation on NRI investments in India is not just possible — it is your legal right. With the right use of DTAA treaties, Foreign Tax Credits, and proper documentation (TRC + Form 10F + Form 67), you can significantly reduce your overall tax burden on Indian mutual funds, fixed deposits, stocks, and dividends.

The key is proactive planning before income is received, not after. Because once TDS is deducted at 30%, recovering it requires ITR filing, processing time, and unnecessary paperwork.

Disclaimer

The content published on NriTaxs is intended for informational purposes only and does not constitute legal, tax, or financial advice. Readers are encouraged to consult qualified professionals before making any decisions based on the information provided.