If you’re returning to India or planning your finances as an NRI, choosing between an RFC Account and an FCNR Account can directly affect your taxes, foreign currency savings, and investment flexibility. Many NRIs assume both accounts serve the same purpose but they’re designed for completely different stages of the NRI journey. In this guide, we’ll compare RFC and FCNR accounts side by side, covering eligibility, taxation, RBI rules, and real-life scenarios, so you can confidently choose the between RFC Account vs FCNR Account based on your residency status and future plans.

What Is an RFC Account?

A Resident Foreign Currency (RFC) Account is a special facility for individuals who return to India after living abroad as NRIs. The key thing to understand is that an RFC account cannot be opened while you still hold NRI status; it becomes available only after you come back to India and qualify as a resident under FEMA.

RFC accounts let returning NRIs continue holding their foreign earnings, NRE balances, and FCNR proceeds in foreign currency instead of converting everything into rupees immediately, which helps avoid currency conversion losses during the transition period. For a complete breakdown of eligibility, documentation, and tax rules, see our detailed RFC Account Guide.

Key Features of RFC Account

- Maintains Foreign Currency Holdings

- Available Only for Returning NRIs

- Flexible Deposits and Withdrawals

- Earn Interest in Foreign Currency

What Is an FCNR Account?

A Foreign Currency Non-Resident, FCNR (B), Account is a fixed deposit that NRIs can maintain in India in foreign currency such as USD, GBP, EUR, AUD, CAD, or SGD. Unlike an RFC account, FCNR deposits are meant for individuals who are still NRIs not residents.

Both the principal and the interest earned on FCNR deposits are tax-free in India and fully repatriable without any limit, which is why FCNR remains one of the most popular parking options for NRIs who want to avoid rupee depreciation risk on their savings.

FCNR deposits are accepted only in fixed maturity buckets between 1 and 5 years; a 6-month FCNR deposit, for example, is not permitted under RBI rules.

Key Features of FCNR Account

- Maintained in Designated Foreign Currencies

- Fixed Deposit Account with Fixed Tenure

- Protection Against Exchange Rate Fluctuations

- Fully Repatriable Principal and Interest

Difference between RFC and FCNR Account

Eligibility

- RFC: Only for individuals who have returned to India and become a resident (or RNOR) under FEMA. Cannot be opened while you are an NRI.

- FCNR: Only for NRIs, PIOs, OCIs, and Indian-origin seafarers who are currently non-resident. Cannot be opened after you become a resident.

Currency

- RFC: Can be held as savings, current, or term deposit, depending on the bank, in major foreign currencies.

- FCNR: Term deposit only, in approved currencies such as USD, GBP, EUR, AUD, CAD, and SGD.

Interest

- RFC: Rates depend on the currency and bank, and are typically linked to global benchmarks rather than domestic FD cycles.

- FCNR: Linked to LIBOR/Swap-based ceilings set by RBI for example, 1–year to under-3-year deposits are capped at the benchmark plus 200 basis points, and 3–5 year deposits at the benchmark plus 300 basis points, though RBI has periodically relaxed these caps for special windows.

Tax

- RFC: Interest is tax-free only while you remain RNOR. Once you become Resident and Ordinarily Resident (ROR), RFC interest becomes fully taxable at slab rates. The payout option (periodic vs. at maturity) matters: periodic interest received during RNOR stays tax-free, but interest accumulated and paid out after RNOR ends can become fully taxable even if it accrued during the RNOR period.

- FCNR: Interest is completely exempt from Indian income tax under Section 10(15)(iv)(fa) of the Income Tax Act, for as long as the depositor holds NRI or RNOR status, right up to maturity or conversion.

Maturity

- RFC: Term deposits under RFC generally have a maximum tenure of 3 years.

- FCNR: Maturity buckets range from a minimum of 1 year to a maximum of 5 years.

Repatriation

- RFC: Principal and interest are generally repatriable, subject to RBI permission and applicable FEMA rules once you are a resident.

- FCNR: Both principal and interest are freely and fully repatriable abroad without any limit, with no special permission needed.

RBI Rules

- RFC: Governed under RBI’s Master Direction on Deposits and Accounts, which treats RFC as a resident account meant specifically for returning NRIs and similar categories.

- FCNR: Governed under RBI’s FCNR(B) deposit regulations, including fixed maturity buckets, premature withdrawal conditions, and periodic interest-rate ceiling circulars (such as the temporary USD/INR swap facility window RBI introduced for 3–5 year deposits in mid-2026).

Risk

- RFC: No exchange rate risk on the foreign currency held, but tax exposure increases once RNOR status ends, so timing your conversion or withdrawal matters.

- FCNR: No exchange rate risk during the deposit tenure since the funds stay in foreign currency, and premature withdrawal before completing one year forfeits all interest.

Best Use Case

- RFC: Parking foreign currency savings, NRE balances, or FCNR maturity proceeds after returning to India, without triggering immediate rupee conversion.

- FCNR: Earning tax-free interest on foreign currency savings while still living and working abroad, with full repatriability when you eventually return or remit funds.

Which One Should You Choose? (RFC Account vs FCNR Account)

| Factor | RFC Account (Resident Foreign Currency) | FCNR Account (Foreign Currency Non-Resident) |

| Who Can Open It? | Returning NRIs (Resident / RNOR status) | Active NRIs, PIOs & OCIs living abroad |

| Primary Purpose | Manage and park foreign currency after moving back to India permanently | Save and grow foreign earnings in foreign currency while living abroad |

| Account Type | Savings, Current, or Term Deposit (FD) | Term Deposit (Fixed Deposit) only |

| Currency Held | Permitted foreign currencies (USD, GBP, EUR, CAD, AUD, JPY, etc.) | Permitted foreign currencies (USD, GBP, EUR, CAD, AUD, JPY, etc.) |

| Deposit Tenure | Highly flexible (depends on the bank/account type) | Fixed tenure ranging strictly from 1 to 5 years |

| Tax on Interest | Tax-Free as long as you maintain RNOR status; becomes taxable once you turn into an ROR. | 100% Tax-Free in India for eligible NRIs during the entire deposit tenure. |

| Repatriation | Fully allowed and unrestricted as per FEMA/RBI rules | Fully repatriable back to your foreign country (both Principal & Interest) |

| Best For… | NRIs returning permanently who want protection against Rupee depreciation | NRIs currently earning abroad who want high-yield tax-free fixed deposits |

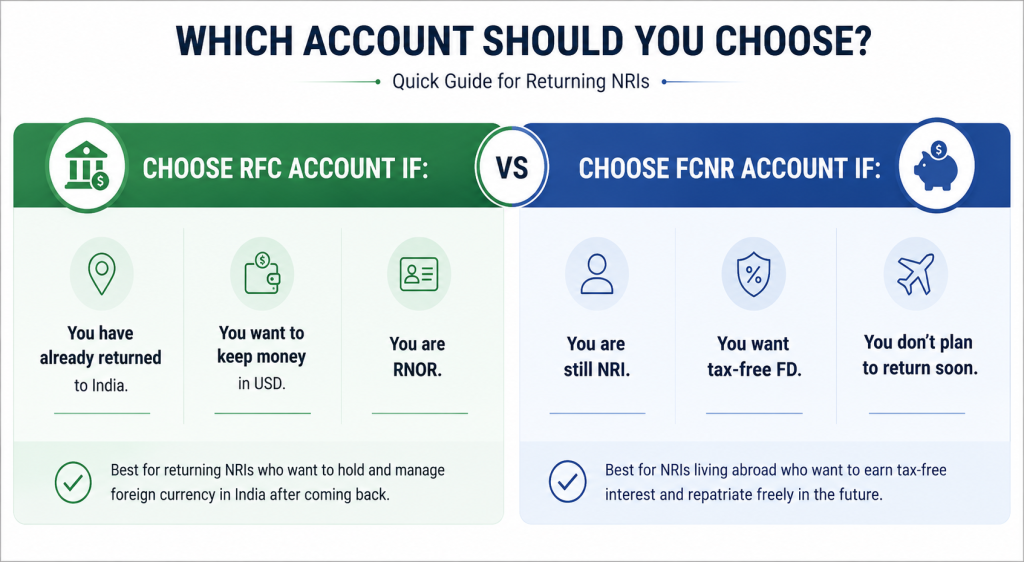

Choose RFC If…

- You have already moved back to India and qualify as Resident or RNOR under FEMA.

- You want to hold your existing foreign currency savings, NRE balances, or FCNR maturity proceeds without converting them to rupees right away.

- You may go abroad again in the future and want the flexibility to repatriate funds later.

Choose FCNR If…

- You are currently an NRI, PIO, or OCI living and earning outside India.

- You want completely tax-free interest in India with zero exchange rate risk while you remain abroad.

- You don’t have immediate plans to return to India and want a fixed-term deposit with full repatriability.

Real Scenarios

Example 1: Raj returned from the USA after 12 years as an NRI and is now classified as RNOR. He still holds a large FCNR deposit that has matured. Since he is now a resident, he cannot renew it as FCNR instead, he converts it into an RFC account, which lets him keep his savings in USD and stay tax-free for the rest of his RNOR period.

Example 2: Priya still works in Canada and has no immediate plans to move back to India. She opens a fresh FCNR deposit in CAD to earn tax-free interest in India while avoiding rupee depreciation risk on her savings, with the comfort of full repatriability whenever she needs the funds.

Taxation: RFC vs FCNR Account

Taxation is the single biggest factor that differentiates these two accounts, and it’s where most NRIs make costly mistakes.

FCNR Taxation

Interest earned on FCNR deposits is fully exempt from Indian income tax under Section 10(15)(iv)(fa) of the Income Tax Act. This exemption continues for the entire tenure of the deposit, right up to maturity, even if you attain RNOR status during that period. However, this exemption applies only in India. Your country of residence may still tax this interest depending on local rules, such as residents of the UK, who are typically taxed on FCNR interest on an arising basis, while UAE residents face no additional tax given the absence of personal income tax there.

RFC Taxation

RFC account interest is taxable in India, but with one important carve-out: if you still hold RNOR status, interest is tax-free as long as it’s received periodically, as and when it falls due. If instead you choose to receive interest only at maturity, and your RNOR status has already ended by then, the entire amount can become fully taxable even though part of it accrued while you were still RNOR. This makes the interest payout option (periodic vs. cumulative) a genuine tax-planning decision, not just a convenience choice.

Once your RNOR period ends and you become a full Resident and Ordinarily Resident (ROR), all RFC interest becomes fully taxable at your applicable slab rate, regardless of payout method. You can also submit a declaration to your bank so TDS isn’t deducted during your RNOR window, which avoids the hassle of claiming a refund later.

RBI Rules Governing RFC and FCNR Accounts

Both accounts are regulated under FEMA and RBI’s deposit and account directions, and a few rules deserve special attention for 2026:

- RFC Accounts are governed by RBI’s Master Direction on Deposits and Accounts and are available only after an NRI becomes a resident under FEMA.

- NRE Accounts must be redesignated as resident rupee accounts once your FEMA residential status changes from NRI to Resident.

- Existing FCNR(B) Deposits are generally allowed to continue until maturity at the contracted interest rate before conversion.

- FCNR(B) Deposits can only be opened for a tenure of 1 to 5 years. Banks cannot offer shorter tenures like 6 months.

- Premature Withdrawal of an FCNR deposit before completing one year results in the loss of interest, and banks may also charge a penalty according to their policy.

- RFC and FCNR Rules are updated periodically by the RBI, including changes to interest rate limits and special facilities. Always verify the latest guidelines before opening or converting an account.

Common Mistakes NRIs Make

Most articles on this topic skip the practical mistakes that actually cost NRIs money. Here are the ones we see most often:

❌ Opening RFC while still an NRI: RFC accounts can only be opened after you become a resident under FEMA. Attempting to open one while still holding NRI status will simply be rejected by the bank, or worse, create compliance issues if misrepresented. Your eligibility also depends on your residential status under Indian tax laws. Learn how the 120-day and 182-day rules determine your NRI, RNOR, or Resident status.

❌ Breaking an FCNR FD early without checking the rules: Premature withdrawal before completing one year means you forfeit all interest entirely, not just a reduced rate. Many NRIs assume they’ll lose ‘some’ interest, not all of it.

❌ Assuming both accounts have the same tax treatment: FCNR interest stays tax-free right up to maturity regardless of your residency timeline within the deposit period, while RFC interest tax-free status depends entirely on your RNOR status and your chosen interest payout method. Treating them as interchangeable can lead to unexpected tax bills.

❌ Choosing cumulative interest payout on RFC without checking RNOR timeline: If your RNOR period is likely to end before maturity, opting for interest paid at maturity instead of periodically can make the entire accumulated interest taxable.

❌ Not informing the bank when residency status changes: FEMA compliance is the account holder’s responsibility. Failing to update your status with the bank when you return to India can create downstream tax and reporting complications.

Conclusion- RFC Account vs FCNR Account

RFC and FCNR accounts solve two different problems at two different stages of your NRI journey. FCNR is built for NRIs who are still living abroad and want tax-free, currency-risk-free returns on their foreign savings. RFC is built for the moment you return to India, letting you hold onto your foreign currency without an immediate, forced conversion into rupees.

The right choice isn’t really RFC versus FCNR as competitors, it’s about picking the right one for where you are right now, and understanding when you’ll need to transition from one to the other. If you’re approaching your return to India, it’s worth speaking with a tax professional about your specific RNOR timeline before deciding on the interest payout option for your RFC account, since that single choice can significantly affect your tax outcome.

Disclaimer

The content published on NriTaxs is intended for informational purposes only and does not constitute legal, tax, or financial advice. Readers are encouraged to consult qualified professionals before making any decisions based on the information provided.