If you’ve recently become an NRI or already live abroad, one of the biggest banking decisions you’ll face is choosing between an NRE Account and an NRO Account.

Many NRIs continue using their resident savings account without realizing that this is not permitted under FEMA regulations once their residential status changes. Others open only one account without understanding the tax implications, repatriation limits, or the purpose of each account.

Choosing the wrong account can lead to:

- Higher taxes on interest income

- Restrictions while transferring money abroad

- Banking compliance issues

- Delays during property sales or rental income transfers

- FEMA-related complications

The good news is that you don’t have to choose only one account. In many cases, NRIs benefit from maintaining both NRE and NRO accounts, each serving a different purpose.

This guide explains everything you need to know about NRE vs NRO accounts in 2026, including taxation, interest rates, repatriation, rental income, salary deposits, FEMA rules, documents required, common mistakes, and how to decide which account is right for your financial situation.

Quick Answer

If your income is earned outside India, an NRE Account is usually the better choice because the interest is tax-free in India and the funds are fully repatriable. If you earn income within India, such as rent, dividends, pension, or property sale proceeds, you generally need an NRO Account to receive and manage those funds.

For many NRIs, the most practical solution is to maintain both accounts.

What is an NRE Account?

An NRE (Non-Resident External) Account is specifically designed for NRIs to park their foreign earnings in India. Money deposited into this account comes from overseas and is converted into Indian Rupees. The biggest advantage is that both the principal amount and interest are freely repatriable and the interest earned is generally exempt from tax in India while you remain eligible under the applicable tax rules.

Key Features

- Only NRIs and PIOs are eligible to open this account.

- Deposits are made in foreign currency (USD, GBP, AED, etc.), which the bank converts to INR at the prevailing exchange rate.

- Available as Savings, Current, Fixed Deposit, or Recurring Deposit.

- Only foreign credits are allowed transfers from other NRE or FCNR accounts, or direct foreign remittances.

- Withdrawals are always made in INR.

What is an NRO Account?

An NRO (Non-Resident Ordinary) Account is meant for managing income generated within India. If you receive rent, pension, dividends, interest, or other Indian-source income, an NRO account is generally the appropriate account for receiving these funds. Unlike an NRE account, the interest earned is taxable in India.

Key Features

- Accepts deposits from both foreign currency and Indian rupee sources.

- Rent, pension, dividends, and interest from Indian investments all flow into NRO.

- Can be held jointly with another NRI or a resident Indian relative.

- Withdrawals are always in INR.

- Repatriation is possible, but with limits and tax implications.

Detailed Difference Between NRE and NRO Accounts

1. Source of Funds

NRE accounts are for parking foreign earnings in Indian currency, while NRO accounts are for Indian-source earnings. This is the most fundamental difference — if the money came from abroad, it goes into NRE; if it was generated in India, it goes into NRO.

2. Taxation on Interest

This is usually the biggest deciding factor. Interest earned on NRE accounts is exempt from tax in India, while interest earned on NRO accounts is taxable as per Indian income tax rules. Specifically, interest earned in an NRO account is taxed at 30 percent, plus applicable surcharge and cess.

3. Repatriation Rules

The principal amount in an NRE account, along with the interest accumulated on it, is fully open to repatriation. In an NRO account, the interest can be repatriated, but the principal can only be remitted up to USD 1 million per financial year.

4. Joint Account Holding

Both NRE and NRO accounts can technically be held jointly with an Indian resident or another NRI — but in practice, NRE joint accounts are mostly held with another NRI, while NRO is popular for joint holding with resident relatives.

5. Deposit Sources

NRE accounts accept deposits only through foreign remittances or transfers from other NRE or FCNR accounts, while NRO accounts can accept deposits from foreign remittances as well as local Indian sources.

6. Exchange Rate Risk

In NRE, foreign currency gets converted to INR every time, so there’s exposure to exchange rate fluctuations. In NRO, since the money (like rent) is already in INR, this risk doesn’t apply.

NRE vs NRO: At-a-Glance Comparison Table

| Feature | NRE Account | NRO Account |

| Full Form | Non-Resident External Account | Non-Resident Ordinary Account |

| Purpose | Parking foreign earnings | Managing India-earned income |

| Funding Source | Only foreign currency / NRE / FCNR transfers | Foreign currency + Indian rupee sources (rent, dividends, pension) |

| Currency Held | INR (foreign currency gets converted) | INR |

| Interest Tax | 100% tax-free in India | 30% TDS + surcharge + cess |

| Repatriation | Fully repatriable (principal + interest) | USD 1 million/year limit, after taxes |

| Joint Holder | Only with another NRI | NRI or resident Indian relative |

| Exchange Rate Risk | Yes (foreign currency → INR conversion) | No (already in INR) |

| Account Types | Savings, Current, FD, RD | Savings, Current, FD, RD |

| Best For | Salary, overseas business income, savings to repatriate | Rent, pension, dividends, income from Indian investments |

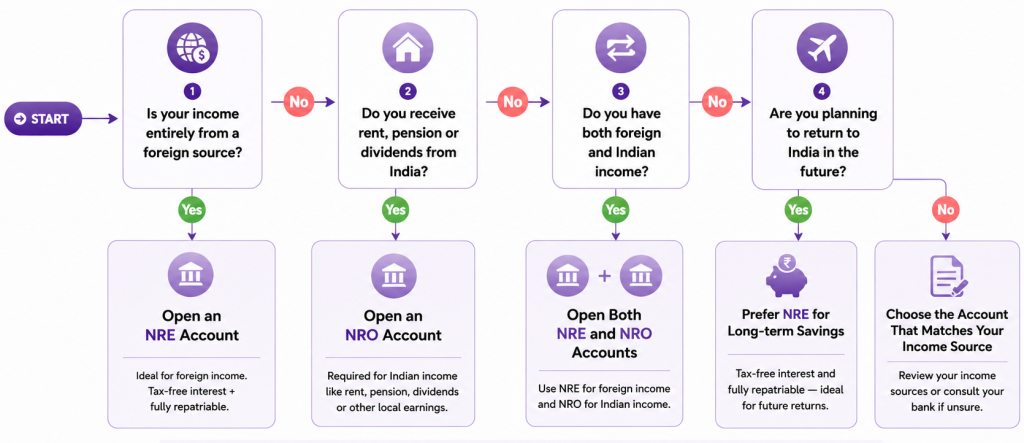

Which Account Should You Choose? (NRE vs NRO Account)

- Only foreign income, no income source in India → NRE is enough.

- Property rent, pension, or dividends come from India → NRO is mandatory.

- You have both income sources (the case for most NRIs) → Open both NRE and NRO.

- Planning to return to India eventually and accumulating savings → Prefer NRE (tax-free + fully repatriable).

- Money from a property sale or investment is already sitting in India → NRO is required (property sale proceeds always get credited to NRO first).

Interest Rates Comparison (2026)

| Account Type | Savings Interest | FD Interest |

| NRE | 3% – 7% p.a. | 6.5% – 8% p.a. |

| NRO | 3% – 7% p.a. | 6.5% – 8% p.a. |

Interest rates on both NRE and NRO savings accounts are broadly similar, ranging from 3 to 7 percent per annum depending on the balance slab and bank policy, while fixed deposits offer 6.5 to 8 percent per annum. The real difference lies in tax treatment NRE FD interest is fully tax-free, while NRO FD interest attracts 30 percent TDS before crediting.

FEMA Rules — Quick Summary

- An existing savings account must be closed or converted to NRO once NRI status begins

- The date your long-term job visa or employment abroad starts is what’s used to calculate NRI status — this is a compliance requirement, not a bank’s discretion

- In practice, NRE becomes the main operating account for foreign income remittance, while NRO functions more like a regulatory income account

RBI Rules — Repatriation & Limits

- NRE: Unlimited repatriation, no documentation hurdles for routine transfers

- NRO: Capped at USD 1 million per financial year, based on proper documentation

- NRO-to-NRE transfers are allowed up to USD 1 million per financial year, after paying applicable taxes and obtaining a Chartered Accountant’s certificate (Form 15CB) — this process is governed by RBI guidelines

Want to understand how NRI taxation works beyond bank accounts? Read our complete guide on How to File Income Tax Return for NRI.

Real-Life Examples: Choosing Between an NRE and NRO Account

Example 1: NRI with Rental Income

Rajesh works in Dubai and owns a flat in Jaipur. His monthly salary is credited to his NRE account, while the ₹18,000 rent from his Jaipur property is deposited into his NRO account because rental income is earned in India.

Key Takeaway: Foreign income belongs in an NRE account, while Indian-source income like rent should be credited to an NRO account.

Example 2: Salaried NRI

Priya, a software engineer in the US, transfers her monthly salary to her NRE account. The funds are converted into INR, the interest earned is generally tax-free in India (subject to applicable rules), and she can repatriate the money abroad without the restrictions that apply to NRO accounts.

Key Takeaway: An NRE account is ideal for managing overseas salary and savings.

Example 3: NRI Returning to India

Amit returns to India permanently after working in the US. Once his residential status changes, he must update his NRE and NRO accounts with the bank. Delaying this update can create banking and tax compliance issues.

Key Takeaway: Inform your bank immediately after your residential status changes.

Example 4: Claiming DTAA Benefits

Meena lives in Canada and earns interest from her NRO fixed deposit. Instead of paying the full TDS rate, she submits a Tax Residency Certificate (TRC) and Form 10F to claim benefits under the India–Canada DTAA.

Key Takeaway: Eligible NRIs can reduce or claim relief from double taxation by using DTAA provisions.

Required Documents (Both Accounts)

- Valid passport

- Visa / work permit / residence permit / OCI card (proof of NRI status)

- Overseas address proof (recent utility bill, bank statement)

- PAN card

- Passport-size photographs

- Initial funding cheque/transfer proof

- For claiming DTAA benefit: Tax Residency Certificate (TRC) + Form 10F

Common Mistakes, FEMA/RBI Rules, Documents & Process

- Continuing to use an old resident savings account — Under FEMA rules, once NRI status begins, a regular resident savings account cannot continue. The system flags it as non-permitted, and the existing account must be closed or converted to NRO.

- Depositing Indian-source income into NRE — Rent, dividends, or even a gift from parents, if deposited into NRE, will get reversed by the bank. Parents in India can deposit rupees into NRO because it’s local money, but that same deposit should not go into NRE, or the bank may reverse the transaction.

- Expecting property sale proceeds directly in NRE — Property sale proceeds are always credited to NRO first. Only after tax calculation and a CA certificate can the funds be transferred abroad. People often expect direct NRE credit, and the payment ends up delayed by weeks.

- Misjudging total income — The bank only looks at the interest amount, not your total yearly income, and automatically deducts 30% TDS. If your total income is below ₹2.5–3 lakh, filing a return gets you a refund.

- Mixing NRE and NRO Demat holdings — As shown in the example above, transfer requests between the two usually get rejected.

Still using a resident savings account? Learn the FEMA rules and penalties for not converting it to an NRO account.

Conclusion: NRE vs NRO Account— The Final Verdict

In simple terms:

- NRE = the home for your foreign income — tax-free, fully repatriable, best for mobility

- NRO = the home for your Indian income — taxable, limited repatriation, but mandatory for any income generated in India

For most NRIs, the right approach is to open both accounts. Use NRE for your overseas savings and salary, and reserve NRO for rent, pension, dividends, and any other India-sourced income. This separation isn’t just tax-efficient — it’s essential for FEMA compliance too. Putting the wrong income into the wrong account can lead to transaction reversals, account freezes, or unnecessary tax burdens.

In 2026, with the Budget’s new TCS cuts, a simplified TDS process, and new investment avenues like GIFT City, NRIs have more options and flexibility than ever before. But all that flexibility only works in your favor once you’ve got the NRE/NRO basics sorted.

Disclaimer

The content published on NriTaxs is intended for informational purposes only and does not constitute legal, tax, or financial advice. Readers are encouraged to consult qualified professionals before making any decisions based on the information provided.