Many Non-Resident Indians (NRIs) incorporate companies in India to explore business opportunities or manage investments. When circumstances change — and the business becomes dormant — simply ceasing operations is not enough. The company continues to exist on paper, accumulating annual filing obligations and potential penalties under the Companies Act, 2013. Formally striking off the company from the Ministry of Corporate Affairs (MCA) register is the only clean, legally sound exit.

This guide explains how NRIs can strike off a company in India, covering eligibility, board resolutions, FEMA compliance, Form STK-2 filing, and the final ROC notification.

What Is Strike Off Of A Company?

Striking off a company refers to the formal removal of its name from the Register of Companies maintained by the Registrar of Companies (ROC). Once struck off, the company ceases to exist as a legal entity and can no longer conduct any business activities or enter into contracts.

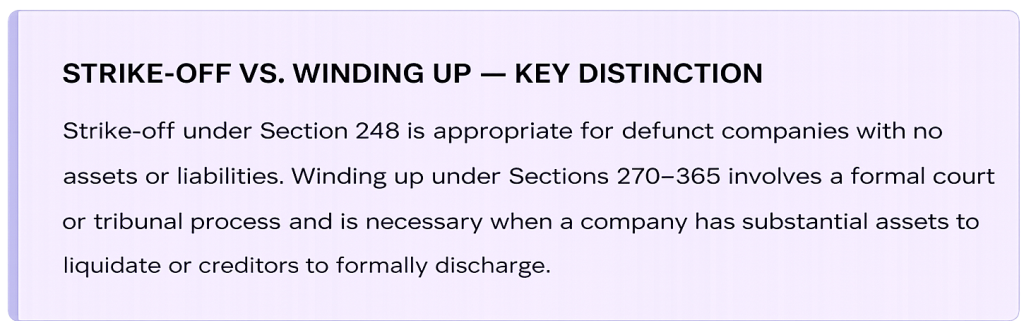

This procedure is governed by Section 248 of the Companies Act, 2013 and is administered through the MCA portal. It is considerably simpler and more cost-effective than winding up, which is a more elaborate legal process reserved for companies with significant assets and liabilities that require formal liquidation through the National Company Law Tribunal (NCLT).

Read Also:- States With No Property Tax For NRIs– Facts, Myths & Investment Insights

Types Of Strike Off Of A Company

There are two distinct routes by which a company’s name can be removed from the Register of Companies. The key difference lies in who initiates the process.

Voluntary Strike Off by the Company

This is the most common and preferable route, where the company’s directors and shareholders collectively decide to close the business. It is available when the company:

- Has not commenced business within one year of incorporation, or

- Has not carried on any business or operations for two preceding financial years, and

- Has no pending liabilities or outstanding statutory dues.

The company proactively files Form STK-2 with the ROC to initiate an orderly, planned closure.

Suo Motu (Compulsory) Strike Off by ROC

In this scenario, the Registrar of Companies initiates the strike-off process on its own accord — hence “suo motu” (Latin: on its own motion). The ROC typically does this when it has reasonable cause to believe a company is defunct, most commonly triggered by failure to file annual financial statements or annual returns for two or more consecutive years.

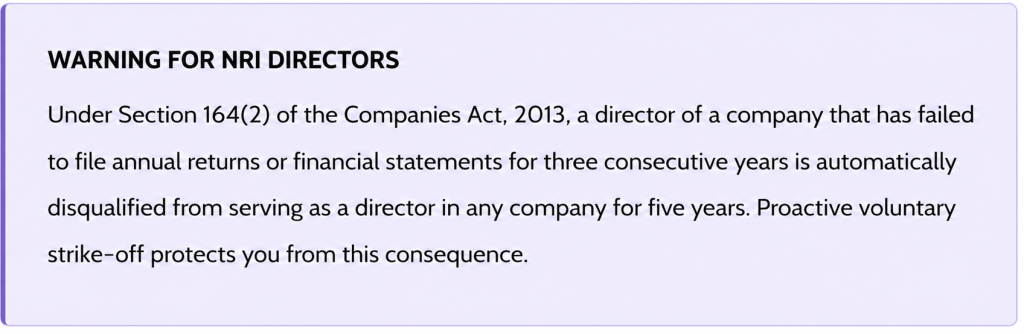

The ROC serves a notice in Form STK-1 to the company and its directors. If no satisfactory response is received, the ROC publishes a public notice and proceeds to strike off the company. For NRI directors, a compulsory strike-off can have serious consequences, including disqualification from directorship in other companies — making voluntary closure always the preferred option.

Eligibility For Nris To Strike Off A Company In India

For a voluntary strike-off application to be accepted by the ROC, the company must satisfy all of the following conditions simultaneously:

- The company is defunct — it either never commenced business within a year of incorporation, or has had no operations for the past two financial years.

- The company has a nil balance sheet — no assets, no liabilities.

- All creditors, employees, and statutory dues (GST, income tax, PF, ESI) are fully settled.

- The company has not changed its name, shifted its registered office, disposed of property, or altered its share capital in the preceding three months.

- The company is not involved in any pending litigation or regulatory proceedings.

- All pending ROC annual filings are up to date or resolved.

Step-by-Step Process: How NRIs Can Strike Off a Company in India

Below is the complete sequence of steps for a voluntary strike-off under Section 248 of the Companies Act, 2013.

Board Resolution

Convene a Board of Directors meeting and pass a board resolution approving the strike-off and authorising one or more directors to handle the application. For NRI directors, the meeting can be held via video conferencing as permitted under Rule 3 of the Companies (Meetings of Board and its Powers) Rules, 2014. Minutes must be properly recorded, signed, and filed.

Clearance of Liabilities

Settle all outstanding dues — creditor payments, employee salaries, GST, income tax, TDS, provident fund, and any other statutory liabilities. Obtain No Objection Certificates (NOCs) from creditors and relevant government departments wherever possible. The company’s bank accounts should also be closed or reconciled to a nil balance.

Extraordinary General Meeting – EGM

Call an EGM of shareholders and pass a special resolution (requiring at least 75% approval by value) to authorise the strike-off. NRI shareholders can participate via proxy or e-voting, depending on the company’s articles of association. Proper EGM notice (21 days) must be issued unless a shorter notice is consented to by members.

Filing of Form MGT-14

Within 30 days of passing the special resolution, file Form MGT-14 with the ROC. Attach a certified copy of the special resolution and the explanatory statement from the EGM notice. This formally records the shareholders’ decision in the ROC’s database. Late filing attracts additional fees.

Filing of Form STK-2

File the primary strike-off application — Form STK-2 — along with: (a) the board and special resolutions, (b) an indemnity bond in Form STK-3 signed by all directors, (c) an affidavit in Form STK-4 from all directors confirming defunct status, and (d) a statement of accounts showing nil assets and liabilities, certified by a Chartered Accountant and not older than 30 days. For NRI directors, all documents signed outside India must be notarised and apostilled.

POC Public Notice

Upon receiving the STK-2 application, the ROC publishes a public notice on the MCA website, in the Official Gazette, and in at least one leading newspaper. This invites objections from any interested party within 30 days. The Income Tax Department, GST authorities, and any creditors may raise objections during this window.

Final Strike-Off Notification

If no objections are received (or all objections are satisfactorily resolved), the ROC publishes a final dissolution notice in Form STK-7 in the Official Gazette. From this date, the company officially ceases to exist as a legal entity. The notification is also available on the MCA portal for public record.

ROC-Initiated (Compulsory) Strike-Off Procedure

When a company fails to file its annual returns (Form MGT-7) or financial statements (Form AOC-4) for two consecutive years, the ROC may initiate strike-off proceedings independently. The ROC sends a notice in Form STK-1 to the company’s registered address and to all directors on record, asking for reasons why the company should not be struck off.

If the company does not respond within the stipulated time — or provides an unsatisfactory response — the ROC proceeds with the same public notice and final gazette notification sequence as in voluntary strike-off. For NRI directors, the risk is compounded because communications may not reach them in time, and director disqualification (Section 164(2)) can occur before any remediation is possible.

Key Compliance Requirements For Nris

NRI-owned companies face additional layers of compliance during the strike-off process due to cross-border investment regulations. Overlooking any of these can delay or invalidate the application.

FEMA and RBI Compliance

The Foreign Exchange Management Act (FEMA) and RBI regulations govern foreign investments in Indian companies. Before closing, verify that:

- All foreign investments were received through proper banking channels (FCNR or NRE accounts) and duly reported to the RBI in the relevant FC-GPR or FC-TRS forms.

- Any repatriation of residual funds after settling liabilities follows RBI’s repatriation guidelines under FEMA.

- A Chartered Accountant’s certificate confirming FEMA compliance accompanies the application.

Income Tax Compliance

All pending income tax returns must be filed, and any outstanding tax demands, interest, or penalties must be cleared. It is strongly advisable to obtain a No-Objection Certificate (NOC) from the Income Tax Department prior to filing STK-2 — this prevents the Income Tax Office from raising an objection during the public notice period.

ROC Annual Filings (MGT-7 and AOC-4)

While the strike-off provision targets defunct companies, the ROC generally expects all pending Annual Returns (Form MGT-7) and Financial Statements (Form AOC-4) to be filed including payment of any late fees before the STK-2 application is accepted. Clearing pending filings demonstrates good faith and avoids procedural rejection.

Digital Signature Certificate (DSC) — Critical for NRIs

All forms filed with the MCA portal, including MGT-14 and STK-2, must be digitally signed. Therefore, it is mandatory for at least one NRI director to have a valid Digital Signature Certificate (DSC). Since DSCs have a limited validity period, NRIs should check if their DSC is active. If it has expired, they will need to renew it, which can take some time due to the verification process for foreign nationals. Planning for this in advance is crucial to avoid last-minute delays.

Documents Required for NRI Company Strike-Off

Document Description |

Form / Reference |

Who Needs It |

NRI / Foreign Director Note |

| Indemnity Bond | Form STK-3 | All Directors | Must be notarised + apostilled if signed outside India |

| Affidavit | Form STK-4 | All Directors | Confirms defunct status; must be notarised + apostilled if signed outside India |

| Statement of Accounts | CA Certified | All | Nil assets & liabilities; must be ≤ 30 days old and certified by an ICAI member |

| Board Resolution | Minutes of Meeting | All | Minutes of Board Meeting (Video conferencing is acceptable) |

| Special Resolution | EGM Minutes + MGT-14 | All | 75% majority; e-Voting or proxy acceptable for NRI shareholders |

| Passport Copy | Self-attested | NRI Only | Identity & address proof; must be notarised (apostille if in Hague Convention country) |

| FEMA Compliance | CA Certificate | NRI Only | Required specifically where foreign investment was involved |

| Income Tax NOC | IT Department | All | Strongly recommended to prevent future objections from the tax department |

| NOCs from Creditors | Creditor Letterhead | All | Required if the company ever had any outstanding creditors |

Cost Of Striking Off A Company In India

The cost of striking off a company in India is relatively modest compared to the penalties for non-compliance. The government fee for filing Form STK-2 is currently INR 10,000. In addition to this statutory fee, there will be professional fees for the Chartered Accountant or Company Secretary who will prepare the documents, provide certification, and manage the filing process. Other costs may include fees for notarization, apostille services, and any expenses related to clearing pending annual filings or tax dues before initiating the strike-off.

Final Thoughts- How NRIs Can Strike Off a Company in India

Closing a company in India as an NRI is a structured and manageable process, provided it is approached with careful planning and attention to compliance. The voluntary strike-off route offers a clean exit for defunct companies, saving directors from the burden of recurring annual filings and potential penalties. As India continues to strengthen its corporate governance framework, the importance of formally closing a non-operational entity cannot be overstated. By following the prescribed steps and ensuring all legal, tax, and regulatory obligations are met, NRIs can dissolve their Indian company smoothly and conclusively.

Disclaimer

The content published on NriTaxs is intended for informational purposes only and does not constitute legal, tax, or financial advice. Readers are encouraged to consult qualified professionals before making any decisions based on the information provided.