For many Non-Resident Indians (NRIs), investing in Indian real estate is a natural choice whether for long-term wealth creation or staying connected to their roots. While buying residential and commercial property is relatively straightforward, agricultural land often raises confusion.

One of the most common questions NRIs ask is: can NRIs buy agricultural land in India? The answer isn’t as simple as a yes or no, because it involves specific regulations, restrictions, and a few important exceptions.

Understanding these rules is crucial, especially since agricultural land in India is governed by strict legal and regulatory frameworks. In this guide, we’ll break down everything you need to know including rules, eligibility, exceptions, and legal ways NRIs can own agricultural land in India.

Can NRIs Buy Agricultural Land in India?

If we talk about Can NRIs Buy Agricultural Land in India then the answer is No, NRIs are generally not permitted to directly purchase agricultural land, farmhouses, or plantation property in India. These restrictions are governed by the Foreign Exchange Management Act (FEMA) and regulated by the Reserve Bank of India (RBI). The rules are designed to control foreign investment in the agricultural sector and protect farmland ownership within the country.

However, this does not mean NRIs cannot own agricultural land at all. They can legally acquire it through inheritance from family members or as a gift from a resident Indian relative, provided all legal conditions are met. So, while direct purchase is restricted, there are still limited and regulated ways for NRIs to hold agricultural land in India.

Read Also:- Can Nris Invest In Mutual Funds In India?

Why NRIs Cannot Buy Agricultural Land in India?

The general prohibition on NRIs purchasing agricultural land is a long-standing policy. This restriction is rooted in several economic and social objectives. The primary goal is to preserve agricultural land for individuals actively engaged in farming within the country. The government aims to prevent speculative investments from driving up land prices, which could make land unaffordable for local farmers and disrupt the rural economy.

Another key reason is to ensure food security and maintain control over the nation’s primary agricultural resources. Allowing unrestricted foreign ownership could lead to land consolidation and a shift in cultivation patterns based on international market demands rather than domestic needs. The legal framework is designed to keep the ownership and cultivation of agricultural land within the hands of resident Indian citizens, thereby supporting the agrarian structure of the country.

FEMA Rules for NRIs Buying Agricultural Land in India

- Under the Foreign Exchange Management (Acquisition and Transfer of Immovable Property in India) Regulations, 2018, NRIs are not allowed to purchase agricultural land, farmhouses, or plantation property in India.

- This rule is issued by the Reserve Bank of India (RBI) and applies to both NRIs and OCI cardholders.

- The restriction is strict and absolute for direct purchase, regardless of the source of funds or country of residence.

- NRIs cannot use NRE or NRO accounts to acquire agricultural land in India.

- Any attempt to buy agricultural land directly is considered a violation of FEMA regulations.

- Such transactions may be declared invalid, and legal action can be taken by authorities.

- Penalties may include financial fines and enforcement action under FEMA laws.

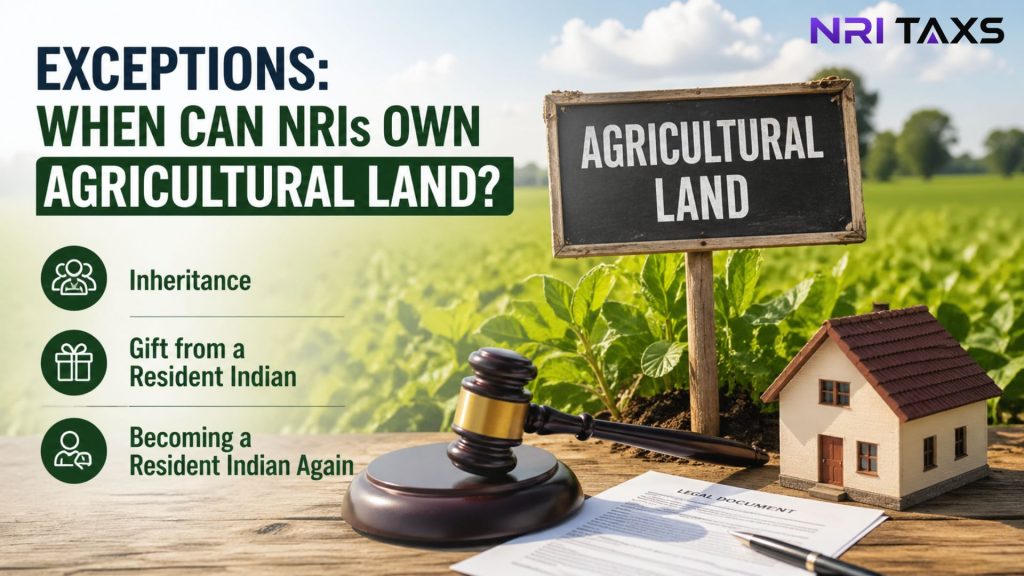

Exceptions: When Can NRIs Own Agricultural Land?

Despite the general prohibition on purchasing, there are specific circumstances under which an NRI or OCI can legally own agricultural land in India. These exceptions are not loopholes but are legally defined channels for property acquisition that do not involve a direct sale transaction.

Inheritance

An NRI or OCI can acquire agricultural land, a farmhouse, or a plantation property through inheritance. This is the most common and straightforward exception. The land can be inherited from any person, whether they were a resident of India or a person resident outside India. The citizenship or residential status of the person from whom the property is inherited does not act as a barrier.

Once inherited, the NRI owner holds all rights to the property. However, the rules regarding the sale or transfer of this inherited land remain applicable. The NRI can continue to hold the property for as long as they wish or cultivate it through legal arrangements. This exception ensures that ancestral property rights are protected regardless of an individual’s current residential status.

Gift from a Resident Indian

An NRI can acquire agricultural land by way of a gift. However, this is subject to a critical condition: the gift must be from a person resident in India who is a close relative. The definition of a “relative” is specified under the Companies Act, 2013, and includes individuals like spouses, parents, grandparents, children, grandchildren, and siblings.

A gift from another NRI or a foreign national is not permitted. The transaction must be properly documented through a registered gift deed to be legally valid. This provision allows for the transfer of family property across generations without involving a commercial transaction, aligning with the policy of keeping land within Indian families while accommodating the non-resident status of a family member.

Becoming a Resident Indian Again

The restrictions under FEMA apply based on an individual’s residential status. If an NRI returns to India with the intention of becoming a permanent resident, their status changes from “Non-Resident Indian” to “Resident Indian” under FEMA definitions. This change is typically determined by the duration of their stay in India during a financial year.

Once their status legally changes to that of a resident, they are no longer subject to the FEMA restrictions applicable to NRIs. As a resident Indian, they can purchase any type of immovable property in India, including agricultural land, without needing any special permission from the RBI. This pathway is available to those who decide to relocate back to India permanently.

Can NRIs Sell Agricultural Land in India?

An NRI who legally owns agricultural land, typically through inheritance or gift, is permitted to sell it. However, the sale is also subject to specific regulations. The most important rule is that the agricultural land can only be sold to a person resident in India who is an Indian citizen.

An NRI cannot sell their agricultural property to another NRI, an OCI cardholder, or any other foreign national. This regulation ensures that the land remains in the hands of Indian residents, reinforcing the original policy objective. The sale proceeds are credited to the NRI’s NRO account. The repatriation of these funds to their country of residence is subject to separate FEMA guidelines and tax obligations.

Tax on Agricultural Land Sale for NRIs in India

The sale of agricultural land by an NRI attracts capital gains tax in India. The tax treatment depends on the holding period of the asset, which determines whether the gain is classified as short-term or long-term.

Short-Term Capital Gains – STCG

If the agricultural land is held for 24 months or less before being sold, the profit from the sale is treated as a Short-Term Capital Gain (STCG). STCG for an NRI is taxed at the applicable income tax slab rates. The calculation is straightforward: the sale price minus the cost of acquisition and any costs incurred for improvement or transfer.

Long-Term Capital Gains – LTCG

If the property is held for more than 24 months, the profit is classified as a Long-Term Capital Gain (LTCG). LTCG is taxed at a flat rate of 20% after indexation. Indexation is a process that adjusts the purchase price of the asset for inflation, which effectively reduces the taxable gain. This benefit makes the tax liability on long-term holdings significantly lower.

Tax Deducted at Source – TDS

When an NRI sells a property in India, the buyer is legally obligated to deduct Tax at Source (TDS). The TDS rate on LTCG is 20%, plus applicable surcharge and cess. For STCG, the TDS rate is 30%, plus surcharge and cess. The buyer must deposit this TDS with the Indian tax authorities and provide a TDS certificate to the NRI seller. The NRI can later claim a refund if their actual tax liability is lower than the TDS deducted.

Risks NRIs Should Avoid While Buying Agricultural Land in India

Given the clear legal restrictions, any attempt to bypass the rules carries substantial risk. NRIs must be aware of common pitfalls and illegal methods sometimes proposed by local intermediaries.

Benami Transactions

One of the most significant risks is entering into a benami transaction. This involves an NRI providing funds to a resident Indian relative or friend to purchase agricultural land in that person’s name. The NRI is the true beneficial owner, while the resident is the legal owner on paper. Such transactions are illegal under the Prohibition of Benami Property Transactions Act, 1988. If discovered, the property can be confiscated by the government, and both parties can face severe penalties, including imprisonment.

Misinterpreting Land Use Classification

Another risk involves the misinterpretation of land records. Some properties may be located in rural areas but may not be classified as “agricultural land” in official records. It is critical to conduct thorough due diligence to verify the exact land use classification from the local revenue authorities. Purchasing land that is later reclassified as agricultural could render the transaction invalid and create legal complications.

Ignoring State-Level Laws

In India, land is a state subject. This means that in addition to central laws like FEMA, each state has its own set of laws governing the ownership and transfer of agricultural land. These state laws may impose additional restrictions, such as land ceiling limits or conditions on who can be considered an “agriculturist.” An NRI must ensure compliance with both central and state-level regulations, which often requires specialized legal advice.

Expert Tips for NRIs Dealing with Agricultural Land

Verify Land Title and Classification:- Before proceeding with any transaction, even a gift or inheritance transfer, conduct a thorough title search. Engage a local lawyer to examine the land records, ownership history, and official land use classification to ensure there are no existing disputes or legal ambiguities.

Understand State-Specific Tenancy Laws:- Each state has unique land reform and tenancy laws. These laws can affect ownership rights, land ceiling limits, and the definition of an “agriculturist.” Familiarize yourself with the specific regulations of the state where the property is located to avoid non-compliance.

Plan for Tax and Repatriation:- If you plan to sell inherited agricultural land, consult with a tax advisor beforehand. Proper planning can help in managing capital gains tax liability and understanding the process and limits for repatriating the sale proceeds under FEMA’s Liberalised Remittance Scheme (LRS) or other RBI-approved routes.

Conclusion- Can NRIs Buy Agricultural Land in India?

The answer to the question, “Can NRIs buy agricultural land in India?” is a clear no. Under the Foreign Exchange Management Act (FEMA), Non-Resident Indians and Overseas Citizens of India are prohibited from purchasing agricultural land, farmhouses, or plantation properties in India. This regulation is consistently enforced to protect the agricultural sector from speculative investment and to preserve land for resident Indian farmers.

However, NRIs can legally own such properties if they are acquired through inheritance or as a gift from a close relative who is a resident of India. They also have the right to sell this legally acquired land, but only to a person resident in India. The legal framework governing these transactions has been stable for many years and is expected to remain consistent into 2026 and beyond, making it essential for all NRIs to adhere strictly to these established rules to avoid severe legal and financial consequences.

Disclaimer

The content published on NriTaxs is intended for informational purposes only and does not constitute legal, tax, or financial advice. Readers are encouraged to consult qualified professionals before making any decisions based on the information provided.