A Health Savings Account (HSA) and a Flexible Spending Account (FSA) are both tax-advantaged accounts designed to help you pay for medical expenses. An HSA is a personal savings account that you own, and it requires you to be enrolled in a High-Deductible Health Plan (HDHP). The money in an HSA rolls over every year and can be invested. An FSA is an account offered by an employer that allows you to set aside pre-tax money for healthcare costs during the year. It typically has a “use it or lose it” rule, meaning funds do not roll over. People often compare them because they both offer tax savings on healthcare spending. The confusion arises from their different rules regarding ownership, eligibility, and what happens to unused funds at the end of the year. So in this blog we will discuss HSA vs FSA for US NRIs.

Introduction Of Health Savings Account

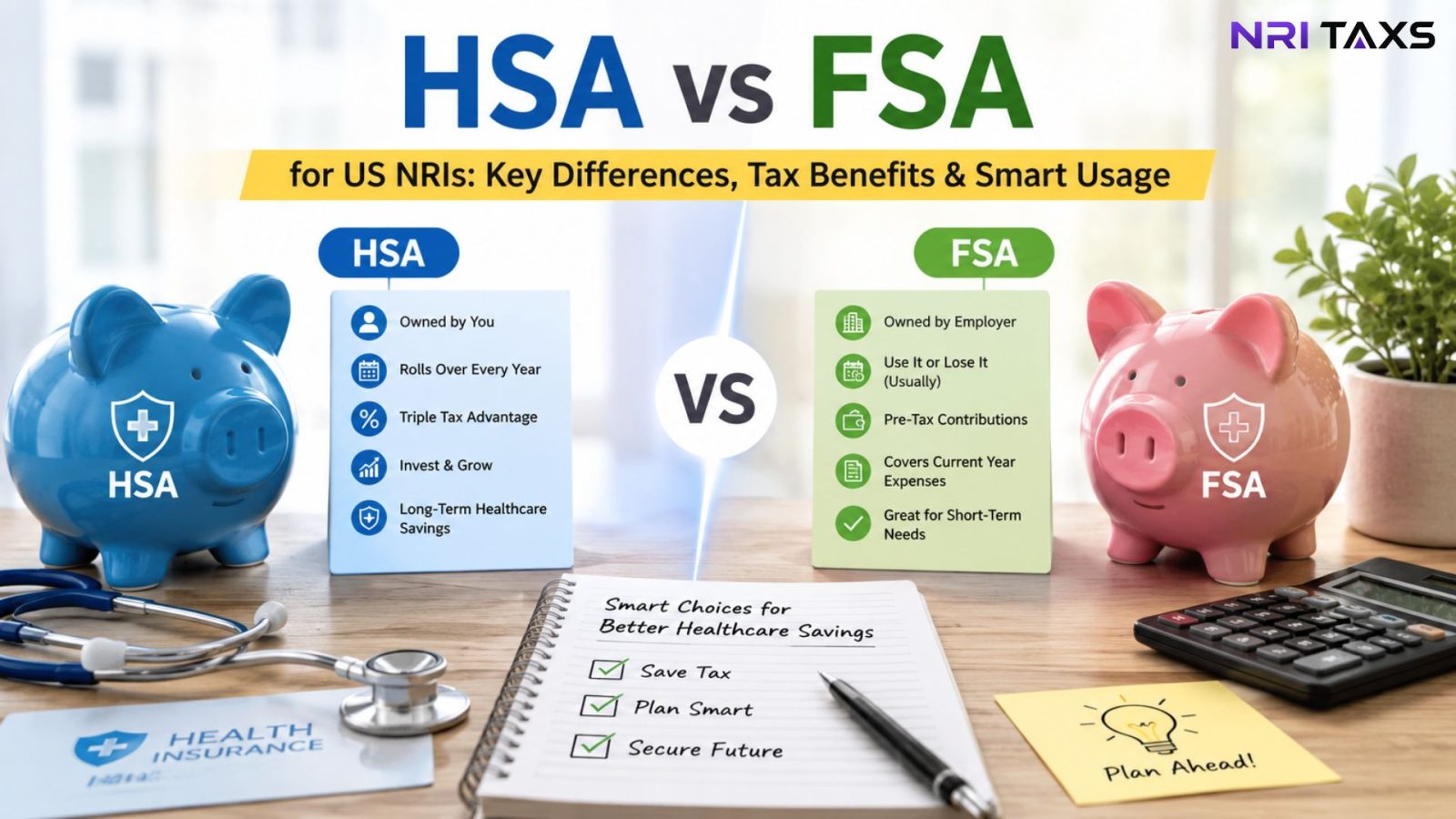

The debate of HSA vs FSA for US NRIsoften begins with understanding each account’s core purpose. A Health Savings Account (HSA) is a tax-advantaged savings account created for individuals who are covered under a high-deductible health plan (HDHP). Think of it as a personal savings account, but the money is specifically for qualified medical expenses. The key benefit is its triple-tax advantage: contributions are tax-deductible, the funds grow tax-free, and withdrawals for medical costs are also tax-free. For example, if you contribute $3,000 to your HSA, you reduce your taxable income by that amount. When you later pay a $400 doctor’s bill from the account, that withdrawal is not taxed. Unlike other accounts, you own the HSA, and the funds never expire.

Features Of Health Savings Account

- Personal Ownership:- Your HSA belongs to you permanently, even if you change jobs, employers, or move to another state or company.

- Lifetime Rollover:- Unused HSA funds never expire and automatically roll over every year, helping you build long-term healthcare savings gradually.

- Investment Option:- HSA money can be invested in mutual funds, stocks, and ETFs to grow wealth alongside healthcare savings over time.

- Triple Tax Benefits:- Contributions, investment growth, and qualified medical withdrawals remain tax-free, making HSA one of the most tax-efficient accounts available.

- Future Healthcare Planning:- An HSA helps cover future medical expenses and retirement healthcare costs without creating additional financial burden later in life.

Introduction Of Flexible Spending Account

A Flexible Spending Account (FSA) is a special account you put money into that you use to pay for certain out-of-pocket health care costs. It is a benefit offered by an employer, and you can only get one through a job. You don’t have to pay taxes on this money. This means you’ll save an amount equal to the taxes you would have paid on the money you set aside.

For example, you decide to contribute $2,000 to your FSA for the year. This amount is deducted from your paychecks in small increments before taxes are calculated, lowering your taxable income. If you then have a $150 dental visit, you can use your FSA funds to pay for it with tax-free dollars.

Features Of Flexible Spending Account

- Employer-Owned Account:- An FSA is linked to your employer, and unused funds are usually lost if you leave your current job.

- Use-It-or-Lose-It Rule:- Most FSA funds must be spent within the plan year, or the remaining balance may expire completely after deadlines.

- Immediate Fund Access:- The full yearly contribution amount becomes available at the beginning of the plan year, regardless of paycheck deductions made.

- No HDHP Requirement:- You can use an FSA without enrolling in a High Deductible Health Plan, unlike Health Savings Account eligibility rules.

- Works With Employer Health Plans:- FSAs are commonly offered alongside employer-sponsored health insurance plans, making healthcare expenses easier to manage using pre-tax income.

Difference Between Health Savings Account And Flexible Spending Account

| Aspect | Health Savings Account (HSA) | Flexible Spending Account (FSA) |

| Eligibility | Must be enrolled in a High-Deductible Health Plan (HDHP). | Offered by an employer; no specific health plan type is required. |

| Account Ownership | You own the account. It is your personal property. | Your employer owns the account. |

| Portability | Portable; the account stays with you if you change jobs. | Not portable; funds are forfeited if you leave your job. |

| Fund Rollover | All unused funds roll over automatically every year without limit. | “Use it or lose it”; most of the balance expires at year-end. |

| Investment | Funds can be invested in stocks, bonds, and mutual funds. | Funds cannot be invested; it is a spending account only. |

| Contribution Limit (2024) | Higher annual limits ($4,150 for self-only). | Lower annual limits ($3,200). |

| Contribution Source | You, your employer, or anyone else can contribute. | Only you and your employer can contribute. |

| Withdrawal Rules | Can be used for non-medical expenses after age 65 (taxed). | Funds can only be used for qualified medical expenses. |

HSA vs FSA for US NRIs: Key Differences

Here are the differences that help you to know HSA vs FSA for US NRIs.

Account Ownership and Portability

A Health Savings Account is a personal asset that you own directly, much like a personal bank account. This means it is fully portable. If you switch employers, retire, or become unemployed, the HSA and all of its funds remain yours. You can continue to use the money for medical expenses and, if eligible, continue making contributions. In contrast, a Flexible Spending Account is owned by your employer. It is tied to your job. If you leave your company, you typically lose access to the account and forfeit any remaining funds.

Fund Rollover

With an HSA, there is no deadline to use your money. Any balance remaining at the end of the year automatically rolls over into the next year and continues to be available for future expenses. This allows an HSA to grow over time into a substantial healthcare fund. An FSA, however, follows a “use it or lose it” rule. You must spend most or all of the money by the end of the plan year. While some employers may offer a short grace period or allow a small rollover amount (around $640 for 2024), you risk losing any significant unused balance.

Eligibility Requirements

Eligibility for these accounts is not the same. To open and contribute to an HSA, you must be enrolled in a qualified High-Deductible Health Plan (HDHP). This is a strict IRS requirement. If you are not in an HDHP, you cannot have an HSA. This makes the account suitable for individuals who are comfortable with a higher deductible in exchange for lower monthly premiums. An FSA is more broadly available. It is an employer-sponsored benefit that can be offered with almost any type of health plan, including traditional PPO and HMO plans. You do not need an HDHP to participate in an FSA.

Investment Potential

Another key factor is the ability to grow the funds. An HSA functions as both a spending and an investment account. Once your balance reaches a certain threshold (e.g., $1,000), you can invest the money in a portfolio of mutual funds, stocks, and bonds, similar to a 401(k) or IRA. This allows your healthcare savings to grow tax-free over the long term. An FSA has no investment feature. It is designed strictly as a spending account. The money you contribute sits in the account as cash and can only be used for eligible expenses; it cannot be invested to generate returns.

Conclusion

Choosing between a HSA vs FSA for US NRIs depends on your health plan, financial goals, and medical needs. An HSA is an excellent long-term savings tool if you are enrolled in a High-Deductible Health Plan. Its portability, rollover feature, and investment options make it ideal for building a healthcare fund for the future. An FSA is better suited for people with predictable, short-term medical expenses who are not enrolled in an HDHP. Its main advantage is providing immediate access to pre-tax funds for the year’s anticipated costs, but it lacks the long-term benefits of an HSA.

Disclaimer

The content published on NriTaxs is intended for informational purposes only and does not constitute legal, tax, or financial advice. Readers are encouraged to consult qualified professionals before making any decisions based on the information provided.